When Chemistry Stops Negotiating

How biofuel mandates, soil degradation, and diminishing reserves are bending the global soybean complex toward a structural breaking point.

Every time a diesel truck fills up with renewable fuel in California, and every time a chicken reaches a dinner plate in Tokyo, those two completely unrelated events are tethered together by an invisible, unbreakable chemical ratio.

The world produces over 420 million metric tons of soybeans every single year. But we don’t really consume soybeans directly. They go through a processing facility called a crush plant. When you crush a metric ton of soybeans, solvent extraction yields 194 kilograms of oil and 785 kilograms of meal. This ratio is the stoichiometry of a chemical process. It does not negotiate. And right now, that rigid biological math is at the center of a slow-motion collision between two of the largest systems civilization depends on: the system that feeds us, and the system that powers us.

Today, we are looking at the hidden geometry of the soybean crush complex. We’re going to look at what happens when a physical system is pushed past its limits, why the safety buffers have essentially vanished, and how climate-driven soil degradation is accelerating a crisis that financial markets cannot simply fix with capital.

Part 1: The Chemical Constraint

To understand the magnitude of what’s happening, you have to understand the bottleneck. Think about the global agricultural system. Usually, if demand for a product goes up, prices increase, and producers make more of it too. But soybeans are weird, they are a joint product.

When a processing plant - a crush plant - takes in raw soybeans, it spits out two distinct commodities. Soybean meal, which is a high-protein powder that makes up nearly 70% of global protein meal consumption for livestock. It feeds pigs, chickens, and cattle. And then you get soybean oil. Traditionally, the oil went into food. It went into salad dressing, frying oil, and margarine.

For decades, this was a relatively stable relationship. Crushers would buy beans, crush them, sell the meal to feed companies and integrators, and sell the oil to the food processors. The revenue from the meal and the oil, minus the cost of the raw beans, is called the gross processing margin, or the crush spread. And for a long time, the meal was the star of the show. 70% of the value of a soybean to a farmer comes from the meal. The oil was almost a byproduct. But because you can’t change the chemistry of a soybean, every decision made on one side of this plant forces a massive consequence on the other.

The plant cannot produce oil without producing meal. It’s physically impossible. In mathematical terms, this is a constraint manifold. You have three separate markets, soybeans, soybean oil, and soybean meal - that trade independently on the Chicago Mercantile Exchange. But chemistry forces them onto a two-dimensional surface. If the price of one moves too far out of line, the physical reality of the crush plant snaps it back.

So, what happens if suddenly, the world decides it needs an astronomical amount of soybean oil, but it doesn’t need any extra meal? Well, you have to crush more beans to get the oil, and as a result, you also produce a mountain of meal and flood the meal market. The price of meal collapses. But you have to keep crushing because the demand for oil is screaming at you to keep going.

That is exactly what’s happening right now. The crush plant is a physical constraint. It is a factory. It runs at capacity. The U.S. crush industry has been operating at over 100% of its installed nameplate capacity. There are no idle plants waiting to be turned on. More capacity requires more infrastructure, and more infrastructure doesn’t appear in months, it takes 2-3 years. So, you have this rigid chemical ratio trapped inside a rigid physical infrastructure. And converging on this bottleneck are two independent, persistent forces.

Part 2: The Demand Shock

The first force is an engineered demand shock, and by engineered, I mean legislated. Over the last few years, soybean oil has been caught up in the energy transition. Governments around the world, but especially in the United States, are heavily incentivizing the production of renewable diesel and biodiesel. Renewable diesel is chemically identical to petroleum diesel, but it’s made from fats and oils - with soybean oil being a primary feedstock.

This isn’t a cyclical trend. It’s a mandated, heavily subsidized structural shift. In the U.S., you have the Environmental Protection Agency setting Renewable Volume Obligations under the Renewable Fuel Standard. You have state programs like California’s Low Carbon Fuel Standard. And you have the transition to the 45Z Clean Fuel Production Credit, which provides massive tax incentives for domestic clean fuel production.

This biofuel transition is qualitatively different from the corn ethanol ramp of 2007–2015. Ethanol demand had substitution pathways and blending flexibility at the retail level — E10, E15, gasoline blending margins could flex. Renewable diesel and biodiesel demand does not have comparable substitution pathways at scale. On-road diesel, off-road diesel, aviation fuel, marine fuel — when the mandate bites, there is no ready substitute waiting in the wings. The soybean oil buffer is compressing in a qualitatively different way than the corn-ethanol buffer ever did, because diesel-side demand is structurally less elastic than ethanol-side demand ever was.

And starting in 2028, the ratchet tightens another notch. Current RFS rules allow imported feedstocks — tallow, used cooking oil, canola, palm derivatives — to claim credits that count toward Renewable Volume Obligations. Starting 2028, that imported share is cut substantially, forcing US domestic origination — meaning US soybean oil — to absorb the shortfall. The same one-way-street dynamic, but now with the import valve closing behind it.

The industry has responded exactly how you’d expect: by building a staggering amount of renewable diesel capacity. According to industry reports, U.S. renewable diesel capacity could reach nearly 8.5 billion gallons per year by 2027. Just in North Dakota, soybean crush capacity practically exploded from zero to 100 million bushels recently, specifically to feed this biofuel boom.

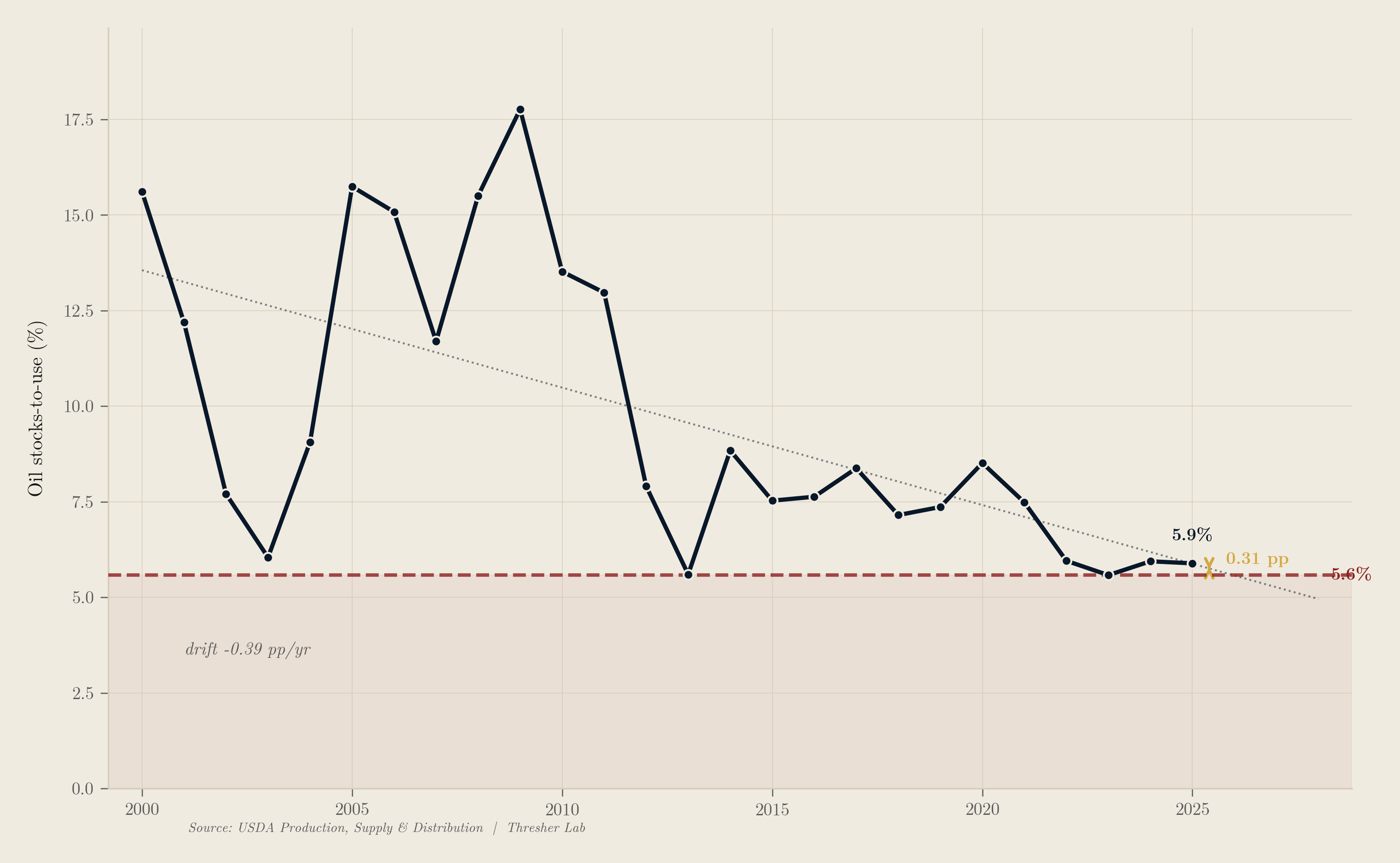

What this means is that the buffer of soybean oil - the safety net of inventory sitting in tanks - is disappearing. Back in the early 2000s, the U.S. had about 43 days of soybean oil supply sitting in reserve. A comfortable 15% stocks-to-use ratio. Today? That buffer has plummeted to about 14 days, hovering near a historical floor under 6%. At higher levels, the stocks-to-use ratio is not even a useful indicator — it becomes a dominant signal below roughly 5.5–6%, where every marginal percentage point of drawdown compresses price response violently. We are inside that high-sensitivity zone now, for the first time in the historical record.

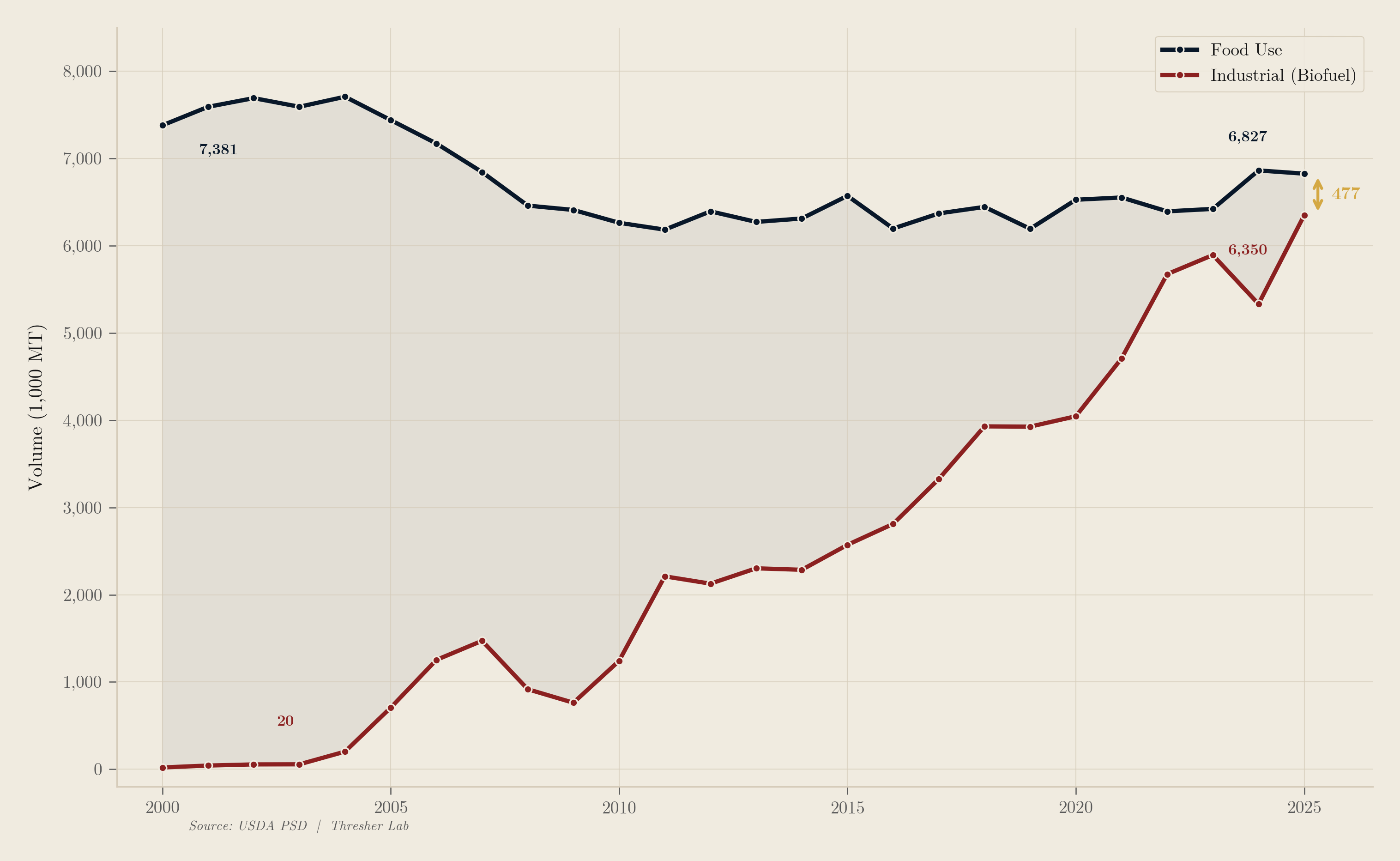

Figure 1. US soybean oil food use versus industrial biofuel use from 2000 to 2025. Food use declined from 7,381 to 6,827 thousand metric tons while industrial use surged from 20 to 6,350, closing the gap to just 477 thousand metric tons.

The share of U.S. soybean oil going to industrial use - which is overwhelmingly biofuels - jumped from just 4 million metric tons in 2020, to well over 6 million. The USDA keeps revising these numbers, projecting over 17 billion pounds of soybean oil could be swallowed up by biofuel production by the 2026-2027 marketing year.

This demand is a one way street. In the language of continuous-time Markov processes, this is a transient force. It doesn’t mean-revert. It just ratchets up, mandated by law, consuming the buffer. When the buffer gets this thin, any tiny disruption in supply doesn’t just cause a ripple; it causes a violent dislocation. The system loses its ability to absorb shocks.

Part 3: The Supply Shock

And that brings us to the second force converging on this bottleneck. While the energy sector is furiously consuming the oil buffer, the environment is degrading the supply base.

If you just look at the headline crop yields for soybeans in the U.S. and Brazil, you might think everything is fine. Yields have gone up over the past few decades, thanks to precision agriculture, better farming practices, and genetically modified seeds. But underneath the surface - literally in the soil - something is breaking.

Soil moisture data across the major soybean producing regions — a fixed network of over a thousand weather stations — shows the soil is losing its ability to hold water. It’s not necessarily that it’s raining less overall. It’s what happens after the rain falls.

Across decades of climate and soil data for U.S. crops, water-holding capacity emerges as the most critical soil property for determining crop yields under heat stress. And the drainage rates at soybean producing sites have been accelerating. The water that feeds the root zones of these plants is leaving the soil about 13% faster than it did twenty years ago.

The soil’s natural buffer against weather variability is thinning. It’s a pedological degradation. And the consequence of this is that weather-driven supply stress episodes - flash droughts, heat waves - are hitting the soybean complex more frequently. In fact, data shows that these stress events are happening 2.2 times more frequently post-2020 than in the preceding two decades.

Structural supply response to a tight soybean balance is constrained by the rotation itself. US farmers in the Corn Belt operate on two-year corn-bean rotations. You cannot plant a significantly larger bean crop in a given year without giving up corn acreage — and corn has its own mandated biofuel demand commitments through ethanol. The rotation puts a structural ceiling on domestic supply elasticity. Even when the signal screams for more beans, the system can only respond at the speed of the crop calendar, one year at a time.

Here’s the really insidious part. This soil degradation is actually being amplified by the biofuel demand we discussed earlier. Think about the feedback loop. Biofuel mandates increase the demand for soybean oil. The crush plants expand to meet that demand. To run those plants you need more soybeans. To get more soybeans, farmers have to plant more acres.

But where do those new acres come from? They increasingly come from marginal lands - lands with poorer soil quality, specifically soils that have a higher fraction of organic matter that degrades quickly under continuous cultivation. These marginal lands are much more vulnerable to rapid drainage and drought stress.

So, the very policy designed to reduce carbon emissions in the transportation sector is driving agricultural expansion onto fragile soils, which accelerates the degradation of the water buffer, triggering more frequent supply shocks, which hits a market with no oil inventory left. It is a perfectly closed, devastating feedback loop.

Part 4: The Geometry of the Squeeze

What happens when these two independent forces - soil degradation from the top, biofuel absorption from the bottom - collide at a processing plant that cannot change its chemistry and is already running at over 100% capacity? The system bends.

In financial terms, this bending shows up in the crush margin. When demand for oil spikes, but a drought hits the fields, the crushers are desperate for beans. The margin violently dislocates. Usually, in financial markets, when a price gets dislocated, capital rushes in to arbitrage it away. If a calendar spread on a futures contract is mispriced, high-frequency traders and hedge funds deploy capital, buy the cheap asset, sell the expensive one, and the gap closes in seconds.

But you can’t arbitrage away a physical constraint with a spreadsheet. When the soybean crush margin bends, it stays bent. It persists. And it persists because the only way to actually close that gap - the only way to restore equilibrium - is to crush more soybeans. But remember, the plants are already full. You need physical capacity. You need a factory.

Capital can’t build a complex solvent extraction facility in 3 days. It takes years. So the margin just sits there, dislocated, screaming a signal that nobody can physically respond to.

In the language of Geometric Arbitrage Theory, this is a failure of the Novikov condition. The market correctly prices the risk - the options market knows exactly how volatile things are - but the arbitrage mechanism is blocked by physical reality. The mathematical integral diverges because the return gap won’t close. And it won’t close because closing it requires steel and concrete, not just liquidity.

The market-clearing mechanism under this constraint is bidirectional and violent. With US domestic biofuel demand price-inelastic — mandated by law — the market doesn’t just shut off US soybean oil exports. It simultaneously bids in every available global feedstock — other vegetable oils, animal fats, used cooking oil — at blown-out spreads. The US Gulf versus Argentina soybean oil spread has widened structurally as a direct consequence. The US becomes a price-inelastic island that must pull in global feedstock supply at whatever cost geography and transportation impose. This is what it looks like when the constraint manifold binds in practice: the entire global flow pattern reorganizes around a single bottleneck.

As the oil buffer gets thinner and thinner, the memory of the system literally lengthens. This is measurable through fractional integration. When the oil buffer is thick - say 10-12% stocks-to-use ratio - the system forgets a shock in a few days. The math shows the fractional integration order is low. But as the buffer approaches that historical floor of 5.6%, the integration order creeps up toward 0.5.

Figure 2. US soybean oil stocks-to-use ratio from 2000 to 2025, declining from 15.6 percent to 5.9 percent. A dashed line marks the historical floor at 5.6 percent, with only 0.31 percentage points of remaining buffer

According to Tauberian theorems, when it hits that point, the system’s auto covariance sum diverges. In plain English: the system loses its ability to forget. A dislocation that used to resolve in a few days now lingers for weeks, because there is no slack left to absorb the stress. When both the supply force and the demand force bind at the exact same time, the half-life of a market dislocation extends by a factor of six.

And let’s look at who bears the brunt of this. The farmer. Historically, 70% of the soybean’s value to a farmer came from the meal. But the crush expansion driven by renewable diesel demand has tilted the value share of the crush toward oil. Meal demand has surprised to the upside — it briefly priced to clear the market, then moved into a regime where meal continues to move without requiring depressed prices. The structural asymmetry is not that meal prices have collapsed. It’s that the margin expansion in the crush is flowing disproportionately through the oil stream, which the farmer does not capture directly. A crop that was historically meal-weighted in farm-gate value now delivers its upside through a component that accrues to the processor and the energy sector, not to the field.

The farmer is dealing with degrading soil, higher input costs, extreme weather, and a structural under-capture of the crush margin — all while the energy sector gets its green fuel. It is a profound structural asymmetry.

The production base is becoming economically unstable at current market prices, essentially maintained by government bridge assistance rather than true economic return. We are approaching a boundary condition. The models that track the memory of these market dislocations are flashing warning signs.

This isn’t just about soybeans. This is a framework for understanding the dynamics of physical systems bound by chemistry. You see it in petroleum refining, where a barrel of crude yields fixed proportions of gasoline and diesel. You see it in base metals smelting, where copper and sulfuric acid come out in fixed ratios. You see it in power grid transmission, where locational marginal prices stay dislocated for years because building a new high-voltage wire takes fifteen years.

We live in a world that assumes financial markets can smooth out physical realities. That capital will magically summon supply. But chemistry doesn’t negotiate. And when you strip away the buffers in the soil and the buffers in the storage tanks, we are left with a raw, exposed physical constraint.

Right now, the global soybean complex is bending under the weight of feeding humanity, and fueling its energy transition simultaneously. The real question isn’t if it’s going to bend further. The question is what happens when it finally hits a point where it can’t bend back and restore equilibrium.

Data & methodology

Measurements & data in this piece draw from USDA Production, Supply & Distribution (oilseeds and oil crops balance sheets), USDA Oil Crops Yearbook, EIA Biofuels Annual, EPA Renewable Fuel Standard program data, Open-Meteo ERA5, and more. The mathematical framework references Geometric Arbitrage Theory, fractional integration models, and Tauberian theorems applied to commodity regime dynamics. Full derivations live in the methodology paper, The Geometry of Soybeans, available on request.